India’s ₹8.2 Lakh Crore Borrowing Target for H1 FY27: Strategic Calm Amid Global Storm

The Borrowing Target That’s Quieter Than It Sounds

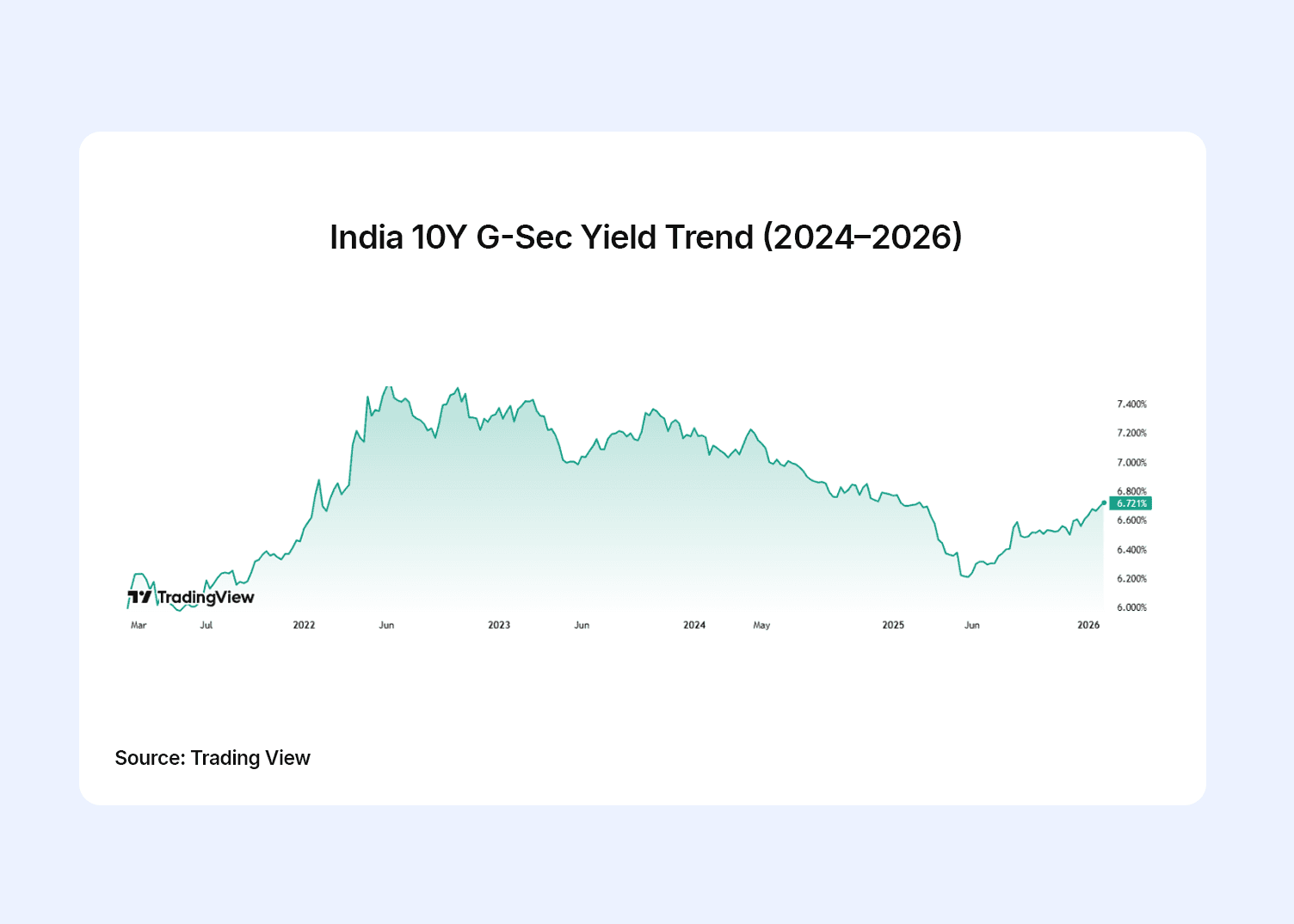

Picture this: Geopolitical tensions in West Asia push India’s benchmark 10-year G-sec yield to 6.94% – its highest in nearly two years. Markets are jittery. Yet, on March 27, 2026, the Finance Ministry drops a calibrated announcement: the Centre’s borrowing target for the first half of FY27 (April–September 2026) is fixed at ₹8.2 lakh crore.

Not a headline-grabbing spike. Not panic borrowing. Instead, a deliberate 51% of the revised full-year gross market borrowing of ₹16.09 lakh crore (down from the Budget’s ₹17.2 lakh crore thanks to smart G-sec switches). This is fiscal policy with a poker face – steady hand in turbulent waters.

As someone who tracks India’s economic pulse from Mumbai’s trading floors (where every basis point move ripples through mutual funds, banks, and retail investors), this borrowing target feels like a masterclass in proactive debt management. It’s not just numbers; it’s a signal that India is prioritising stability over speed.

What Exactly Is the H1 FY27 Borrowing Target?

The ₹8.2 lakh crore will be raised through 26 weekly auctions of dated securities spanning 3 to 50 years. The plan includes ₹15,000 crore in Sovereign Green Bonds (SGrBs) to fund climate-friendly projects.

Here’s the maturity-wise breakdown (a shift from heavy ultra-long issuance in recent years):

| Maturity | Share of Borrowing |

|---|---|

| 3-year | 8.1% |

| 5-year | 15.4% |

| 7-year | 8.1% |

| 10-year | 29% |

| 15-year | 14.5% |

| 30-year | 7.3% |

| 40-year | 8% |

| 50-year | 9.6% |

Source: Finance Ministry release (via Economic Times). Note the reduced tilt toward 30-50 year papers – a conscious move to avoid locking in high yields for too long.

The RBI has also hiked the Ways and Means Advances (WMA) limit to ₹2.5 lakh crore for H1, giving the government breathing room for short-term cash mismatches without flooding the market.

This borrowing target directly funds the fiscal deficit projected at 4.3% of GDP for FY27 – a marginal improvement from FY26’s revised 4.4%. Net market borrowings for the full year are pegged at ~₹11.7 lakh crore, with the rest from small savings and other sources.

How Does This Compare to Previous Years?

India has historically front-loaded borrowing to kick-start capex early. Let’s put the current plan in perspective:

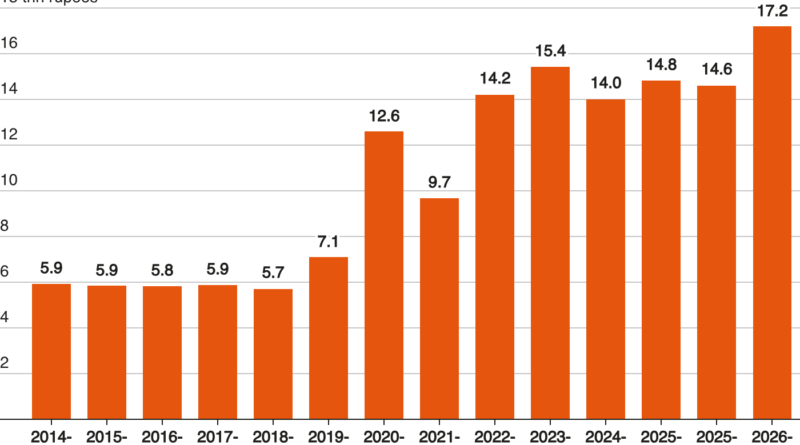

| Fiscal Year | Annual Gross Borrowing (₹ lakh cr, Budgeted/RE) | H1 Borrowing (₹ lakh cr) | H1 as % of Annual |

|---|---|---|---|

| FY26 | 14.82 (Budgeted) | ~8.00 | 54% |

| FY27 (Revised) | 16.09 | 8.20 | 51% |

| FY27 (Original BE) | 17.20 | – | – |

Key takeaway: This is the least front-loaded H1 programme in recent memory. Previous years saw 53-56% in the first six months to front-load expenditure. The government is consciously holding back ~₹0.3-0.5 lakh crore for H2, buying time until global uncertainties (read: West Asia conflict) ease.

This isn’t weakness – it’s wisdom. In FY26, heavier early borrowing coincided with relatively stable global conditions. Today, with yields spiking 26 bps in a month, a lighter footprint prevents crowding out private investment and keeps borrowing costs in check.

Government Bonds Interest Rates Explained: What Drives G-Sec Yields in India

(India 10Y G-Sec Yield Trend 2024-2026 – the recent spike is visible, making the calibrated borrowing even more timely.)

Key Insights: Why This Borrowing Target Matters for India’s Economy

1. Bond Market Relief Economists like Aditi Nayar (ICRA) and DK Pant (India Ratings) call it “judicious.” Less supply pressure in a high-yield environment should help cool the 10-year benchmark. If the conflict de-escalates, H2 borrowing can be executed at lower costs. Traders in Mumbai’s G-sec desks are already breathing easier.

2. Green Finance Push The ₹15,000 crore in Sovereign Green Bonds isn’t tokenism. It’s part of a growing pipeline – India has steadily scaled SGrBs to attract ESG capital and fund renewable energy, electric mobility, and climate resilience. For investors, these often carry a “greenium” (slightly lower yield) but align portfolios with India’s net-zero ambitions.

Sovereign Green Bonds : Work, Interest Rates, Examples & Benefits – GeeksforGeeks

(Infographic on benefits of Sovereign Green Bonds – a visual reminder of how this borrowing target doubles as sustainable finance.)

3. Fiscal Prudence in a Debt-to-GDP World India has shifted its anchor from pure deficit targets to debt-to-GDP (projected 55.6% for FY27, aiming for 50% by 2031). This borrowing target reflects that discipline: switches reduced the ask by ~₹1.11 lakh crore post-Budget. It signals to rating agencies and global investors that capex (₹12.2 lakh crore in Budget) won’t derail consolidation.

4. Implications for You – The Investor in Mumbai (or Anywhere)

- Bond Investors & MFs: Expect potential yield compression in H1. Duration funds could benefit if the plan succeeds.

- Equity Markets: Lower government borrowing pressure = less crowding out of corporate bonds = easier liquidity for capex-heavy sectors like infra and renewables.

- Retail Angle: If you hold debt mutual funds or are eyeing tax-free bonds/small savings, watch for indirect spillover. Higher WMA also means RBI has tools to manage liquidity without aggressive rate hikes.

- Broader Economy: Stable borrowing supports the 6.5-7% growth narrative without stoking inflation or rupee volatility.

From my lens analysing reams of fiscal data, this feels like India learning from past cycles – avoiding the “borrow first, ask questions later” trap that amplified yield spikes in 2022-23.

The Road Ahead: Prudence as Competitive Edge

This borrowing target isn’t flashy, but it’s foundational. In a year when global bond markets face Trump-era uncertainties, Middle East flare-ups, and Fed recalibration, India is choosing flexibility over front-loading. It buys time, protects yields, and keeps the green finance engine humming.

Will yields actually cool? Will H2 borrowing be even lighter if peace returns? Markets will vote with their bids in the first 26 auctions. But one thing is clear: the Centre is playing the long game – fiscal consolidation with strategic restraint.

What’s your take? Does this calibrated borrowing target reassure you about India’s debt trajectory, or do you see risks if global shocks persist? Drop your thoughts in the comments below. If you found this breakdown useful, hit subscribe for more deep dives into Budget moves, bond strategies, and green finance. And don’t miss our companion piece on “How Sovereign Green Bonds Are Reshaping India’s Capex Story.”

Stay informed. Stay invested. India’s fiscal playbook just got a smarter chapter.